Checking a policy renewal is easy. Checking it well is where the risk of an E&O lawsuit hides.

In most commercial insurance agencies, Account Managers and CSRs still dread the arrival of a renewal policy document. The process hasn't changed in decades: open the 120-page expiring policy PDF, open the 120-page new renewal PDF, and begin the agonizing process of a side-by-side visual comparison.

The policy eventually gets presented to the client—but at what risk?

This article explores how an AI Policy Variance Finding Agent automates the comparison process to eliminate administrative grunt work, guarantee 100% accuracy, and protect your agency from catastrophic E&O (Errors & Omissions) claims.

If your agency relies on human eyes to catch silent coverage reductions buried in dense legal text, this blog explains where the critical failure point is—and how AI fixes it.

1. The Ground Reality Inside Policy Checking

For every commercial renewal, the agency has a fiduciary duty to ensure the client’s coverage hasn’t quietly eroded year-over-year. Carriers frequently update their forms, adding new exclusions, changing deductible structures (e.g., from flat dollar to percentage), or reducing specific sub-limits.

When that 120-page renewal PDF arrives, an Account Manager who is already managing 50 other active renewals is expected to proofread the legal dense legal text.

Under time pressure, they inevitably focus only on the main declarations page: Is the premium correct? Are the main limits the same?

The remaining 110 pages of endorsements, exclusions, and definitions get a cursory scan. This is where the "silent variance" is missed, and where agency liability is born.

2. Why Manual Policy Variance Finding Breaks at Scale

The traditional policy checking process is broken because it relies on human eyes to perform a machine-level task. When an Account Manager is forced to "spot the difference" across two 100-page legal contracts, human fatigue isn’t a performance issue—it’s a mathematical certainty.

The data behind manual policy auditing reveals a dangerous gap in agency operations:

- The 90-Minute "Deep Read" Requirement: Industry experts estimate that to truly audit a mid-market commercial policy for all form changes and endorsements, it requires 90 to 120 minutes of uninterrupted focus. In a high-volume agency, AMs rarely have more than 15 minutes per policy, creating a 75-minute "blind spot" in every renewal.

- The 1-in-10 Error Rate: Internal audits of manual policy checking shows that even experienced CSRs miss 10% to 15% of "non-premium" changes—such as a shift from a "per occurrence" to a "per claim" trigger or a new sub-limit on transit coverage.

- The $40,000 E&O Deductible: The average cost of an Errors & Omissions (E&O) claim is rising, but the immediate hit is the deductible. For many mid-sized agencies, a single missed exclusion can trigger a $25,000 to $50,000 out-of-pocket deductible before the insurance even kicks in.

Humans are naturally good at finding big changes (like a $5,000 premium hike) but biologically poor at finding "small" textual shifts. If a carrier changes a definition from "including but not limited to" to just "including," a human eye will skip right over it. However, that one-word shift can be the difference between a covered $1M loss and a total denial. At scale, relying on "spot checking" is effectively gambling with the agency’s balance sheet.

High-level Account Managers are hired for their relationship skills and technical expertise, yet they spend 20% of their annual billable hours acting as proofreaders. This "clerical drag" doesn't just increase your G&A (General and Administrative) expenses; it leads to top-tier talent burnout. When your best people are buried in PDFs, they aren't out defending your book against competitors.

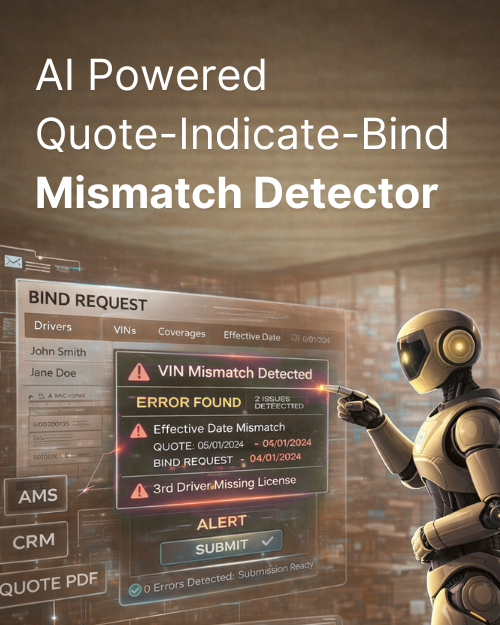

3. What an AI Policy Variance Finding Agent Actually Is

An AI Policy Variance Finding Agent is an autonomous precision engine that sits between your Agency Management System (AMS) and your incoming carrier documents.

It does not replace your Account Managers. Instead, it reads both policy PDFs—the expiring one and the renewal—and understands insurance terminology.

It instantly extracts thousands of data points and generates a single-page "Variance Report" highlighting every single difference, no matter how small or deeply buried.

Your team stops acting as proofreaders and starts acting as risk advisors.

4. How the AI Agent Works (System-Level View)

- Step 1: Document Ingest: The agent monitors the AMS or a designated email inbox for bound renewal policies. It automatically identifies the corresponding expiring policy document from the client file.

- Step 2: AI-Powered OCR & Parsing: The AI doesn't just treat the PDF as an image; it reads the text. It uses large language models (LLMs) trained specifically on insurance contracts to understand the structure, provisions, definitions, and clauses in both documents.

- Step 3: Deterministic Comparison: The agent performs a side-by-side digital comparison. It maps data points: Expiration Policy - Liability - Aggregate Limit ($2M) vs. Renewal Policy - Liability - Aggregate Limit ($2M). It repeats this for deductibles, exclusions, conditions, and endorsements.

- Step 4: Variance Report Generation: The AI creates a simplified, one-page report. It ignores what matches and exclusively flags the variance. For example: "Property Deductible changed from $5,000 Flat to 2% of Total Insured Value." This report and both PDFs are synced back to the AMS for the AM’s immediate review.

Free Session with Our Head of AI

30-Minute, no-strings-attached brainstorming session to identify potential bottlenecks and explore how AI can solve your business challenge.

Book Now →.png)

5. A Realistic Agency Example

Consider an agency with 200 commercial renewals a month, involving complex risks like real estate schedules or manufacturing.

Before AI, checking these policies takes Account Managers roughly 45 to 60 minutes per policy. That is over 150 hours a month of high-paid staff time spent staring at PDFs.

Worse, in 10% of the cases, major changes (like a new "Assault & Battery" exclusion in a hospitality policy) are completely missed until a claim is denied. The agency lives in constant dread of an E&O lawsuit.

After implementing an AI Policy Variance Finding Agent, the Account Manager is alerted to a new bound renewal. They open the system and are presented with a concise, generated Variance Report.

It highlights two changes: a sub-limit reduction on cyber coverage and a change in the wind/hail deductible definition.

The AM reviews the report in 5 minutes, contacts the carrier to negotiate, and advises the client of the changes. The agency reclaims 130 hours a month and eliminates the E&O risk.

6. Before vs After: Policy Checking

.png)

7. KPIs That Move After Implementation

Agencies using AI Policy Variance Finding Agents see immediate improvements in operational hygiene:

- Less Hours spent on policy checking per renewal

- Reduces E&O liability risk rating

- Increased Percentage of renewals checked (move from spot-checking to 100% check)

- High Account Manager job satisfaction (elimination of hated task)

But the most critical metric is this:

E&O exposure per $1M of commission revenue.

When you automate the process, that metric drops to zero.

8. Who Should Deploy AI Policy Checking First

This use case delivers the absolute highest ROI for agencies managing large commercial lines (middle-market and up), where policies are complex, customized, and high-premium.

If your agency handles complex property schedules, construction risks, or liability policies where endorsements change frequently, this agent is not a luxury; it is a critical defensive system for your business.

Free Session with Our Head of AI

30-Minute, no-strings-attached brainstorming session to identify potential bottlenecks and explore how AI can solve your business challenge.

Book Now →

9. Common Objections (and Reality)

- "Will it understand carrier-specific endorsement language?" Yes. The LLMs used are pre-trained on the exact legal and operational definitions used across the entire insurance industry, not just general language.

- "Can I trust the AI to write the final report?" The AI generates the draft of the report, highlighting the data variance. The Account Manager remains the advisor. They must still review the agent's findings, decide if they need to negotiate with the carrier, and explain the changes to the client. The AI does the grunt work; the human makes the decision.

- "Our CSRs are already trained to check policies." They are trained, but they are human. They will miss things. Training cannot solve human eye glaze.

10. The Bigger Shift: From Proofreading to Advising

Traditional agency workflows treat policy checking as a purely administrative clerical task—a time-consuming tax on renewal revenue. AI reframes it as a high-value advisory function.

When your team spends zero time hunting for changes, they can spend 100% of their time advising the client on why those changes matter and how to mitigate the risk.

The goal is not just to check a policy; it is to master the risk. In the modern insurance landscape, eliminating clerical grunt work so you can deliver expert-level advice faster than the competition is how you win.

Ready to eliminate your agency’s E&O risk and reclaim hundreds of hours of staff time?

Booking a strategy call with our Head of AI is the fastest way to see exactly how this fits into your tech stack and map out your custom implementation plan.

.png)

%20for%20insurance%20agencies.png)

.png)

Christian Financial Credit Union

Huntington National Bank

Paqqets

Meridian Medical Management

Thales Group

Meridian Medical Management